Historically the ATO has been able to issue lockdown Director Penalty Notices for unpaid amounts of superannuation if SGC Statements have not been lodged within three months of superannuation being due for payment.

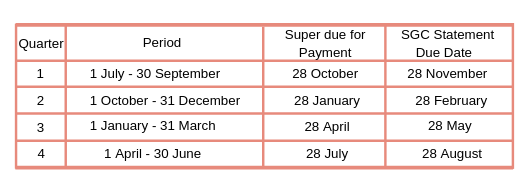

However, in May 2019 legislation came into effect, which shortened the period for lodgement of SGC Statements in order to avoid lockdown Director Penalty Notice liability. As a result of this legislation lockdown Director Penalty Notices can now be issued if SGC Statements are not lodged by the SGC Statement Due Dates as set out below:

Lockdown Director Penalty Notices

If a lockdown Director Penalty Notice is issued, a director can only avoid liability under the notice by arranging for the superannuation to be paid to the ATO by way of Superannuation Guarantee Charge. Appointing a liquidator or voluntary administrator to a company will not avoid liability for lockdown Director Penalty Notice amounts and the ATO can:

- Issue lockdown Director Penalty Notices after a company is placed in liquidation or voluntary administration; and

- If necessary, base lockdown Director Penalty Notices on estimates of a company’s superannuation liability.

What Happens if SGC Statements are Lodged by the Due Dates?

If superannuation is not paid but SGC Statements are lodged by the relevant due dates, then a director can avoid liability by appointing a liquidator or voluntary administrator to a company. This must be done either before a Director Penalty Notice is issued or within 21 days of the date of the Notice. In these circumstances the ATO cannot issue a Director Penalty Notice after the date of a liquidator’s or administrator’s appointment.

Advice and Assistance

Given the serious effects the Director Penalty Notice regime may have on company directors’ personal financial positions, directors and their advisors should obtain appropriate advice and assistance if a company is failing to pay superannuation or PAYG Tax.

If you would like to obtain professional advice regarding your circumstances, please contact Pearce & Heers at our Brisbane or Gold Coast offices for an initial obligation-free consultation.