We are commonly asked to assist people involved in a business that has failed. Often one of the impacts of the business’ failure is that a bank loan to the business has not been paid. This loan is also often guaranteed by the person running the business but also by his or her partner, with the loan being secured over a jointly owned property.

The bank is obviously going to want to be repaid this loan and it will likely be entitled to take any steps necessary to recover the debt. But what happens to any remaining equity in the property then? And how will this impact the co-owner of the house who was not involved in the business?

What is the doctrine of equitable exoneration?

The doctrine of equitable exoneration will apply in circumstances where two people give security, but only one person has benefited from the loan. For example, it may apply if the loan was for a business traded by a company of which only one person was director and shareholder. In these circumstances the person for whom the loan has no benefit is deemed only to be acting as surety or guarantor to the loan and the security that person has given is only to secure their obligations as surety.

In very simple terms, this means the person who is the director and shareholder of the company should in the first instance be the one who has to repay the loan.

How does this work if a property is involved?

If a loan is secured over property, when the loan is repaid it should first be repaid from the sale proceeds from the interest in the property owned by the director and shareholder of the company. Naturally if the director’s interest in the property is insufficient to pay the loan, then the bank will be able to be paid from the co-owner’s interest.

When can this be important?

This can be important when it is likely that the director and shareholder of a company will go bankrupt, which can often be as a result of other debts owed. In these circumstances, if the doctrine of equitable exoneration applies then the director’s Bankruptcy Trustee may have no interest in a property owned by the director and his or her partner.

How does this work in practice?

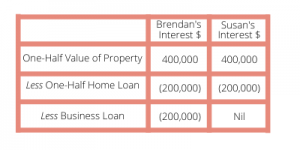

Let’s assume Brendan is the sole director and shareholder of a company, which goes into liquidation with a debt of $200,000 owing to the Bank. Brendan and his wife Susan jointly own a house worth $800,000, which is subject to an ordinary home loan of $400,000. Applying the doctrine of equitable exoneration then the respective interests in the house are:

Therefore, applying the doctrine of equitable exoneration Brendan has no interest in the house and Susan is entitled to either the whole property (although she will still have to pay all loans) or if the property is sold all of the equity.

Advice and assistance?

If you are in a similar situation and would like to understand how Equitable Exoneration may effect you or your partner, please contact Pearce & Heers at our Brisbane or Gold Coast offices for an for an initial, obligation-free consultation.