The ATO can issue a Director Penalty Notice to recover a company’s unpaid PAYG Tax, GST and superannuation from a company’s directors.

There are two types of Director Penalty Notice the ATO can issue. They can apply as follows.

21-Day DPN – PAYG Tax, GST or Superannuation Unpaid but Returns Lodged Within Relevant Periods

A company is required to:

- Pay PAYG Tax and GST to the ATO by due dates.

- Lodge Business Activity Statements (“BAS”) with the ATO each quarter reporting PAYG Tax and GST payable.

- Pay superannuation by due dates.

- If the company doesn’t pay superannuation by due dates, lodge a Superannuation Guarantee Charge Statement (“SGC Statement”) with the ATO.

Where a company doesn’t pay PAYG Tax, GST or superannuation, but it lodges its BAS within 3 months of being due and SGC Statements when due, the ATO can issue a Director Penalty Notice to the company’s directors. If this happens directors can be liable for the PAYG Tax, GST or superannuation claimed. However, directors can avoid personal liability if:

- The PAYG Tax, GST or superannuation is paid; or

- The company is placed in liquidation or voluntary administration within 21 days of the date of the Director Penalty Notice.

“Lockdown” DPN – PAYG Tax or Superannuation Unpaid and Returns not Lodged Within Relevant Periods

“Lockdown” Director Penalty Notices apply where a company doesn’t pay PAYG Tax, GST or superannuation. And also doesn’t lodge BAS within 3 months of being due or SGC Statements by required dates. If this occurs the directors are automatically liable for PAYG Tax, GST or superannuation and:

- The ATO can issue a Director Penalty Notice to recover unpaid PAYG Tax, GST or Superannuation.

- Placing the company in liquidation or voluntary administration doesn’t avoid liability. The ATO can issue Director Penalty Notices after a company is already in liquidation or voluntary administration.

- The ATO can estimate a company’s debts for PAYG Tax, GST and superannuation. After estimating the debts the ATO will issue a Director Penalty Notice based on estimates.

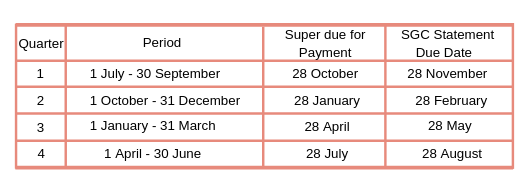

In May 2019 legislation was passed to change the date which a company must lodge SGC Statements for directors to avoid being automatically liable for SGC debts. The dates for lodgement of SGC Statements to avoid liability are now:

What Happens if You are Liable Under a Director Penalty Notice?

If you become liable under a Director Penalty Notice the ATO will treat the debt as it would treat any ordinary tax debt . The ATO can and will:

- Commence legal proceedings against you to obtain a Judgment for the amount of the debt.

- Use the Judgment to issue a Bankruptcy Notice and then subsequently make you bankrupt.

- Garnishee funds from your personal bank account or from your wages.

If a company has multiple directors, the ATO will often target its recovery action at the director it considers has the best ability to pay. The ATO will have information on a director’s personal financial position based on the director’s past Income Tax Returns.

What Can You Do to Avoid Director Penalty Notice Debts?

The following tips will help you avoid liability under Director Penalty Notices:

- Obtain advice at an early stage. If you call us we can advise on risks associated with the continued trading of your company.

- Lodge BAS and SGC Statements on time or at worst within the timeframes set out above. If lodgements are made but tax debts are not paid you still have 21 days from the date of a Director Penalty Notice to place a company in liquidation or voluntary administration to avoid liability.

- Make sure your postal address is up to date in records maintained by ASIC. Director Penalty Notices are issued to your personal address as recorded with ASIC. If you do not receive a notice due to a change of address this is not a defence to a claim by the ATO.

- If a liquidator or administrator is to be appointed, the time to make an appointment is within 21 days of the DATE of the Director Penalty Notice.

- If a Director Penalty Notice is received act promptly in obtaining advice from a qualified professional.

What Can You Do if You are Liable to Pay a Director Penalty Notice?

If you are liable under a Director Penalty Notice then:

- You should promptly obtain advice from a qualified professional.

- You can negotiate a personal payment arrangement with the ATO for the amount of the director penalty debt. We have assisted numerous company directors negotiate these types of payment arrangements.

- If there are other directors of the company, seek that they make a contribution to the ATO to pay a proportionate part of the liability.

- Consider whether it may be possible to put forward a proposal for a Personal Insolvency Agreement.

- If there are no other alternatives, consider filing for bankruptcy.

Old and New Directors

The ATO can issue a Director Penalty Notice to a director who was a director at the time when unpaid PAYG Tax or superannuation was incurred, but who has subsequently resigned.

The ATO can also issue a Director Penalty Notice to an incoming new director. Whilst the director is liable immediately the ATO cannot issue a notice until the director has been in office for more than 30 days.

Defences to Claims by the ATO Under Director Penalty Notices

A company’s director will have a defence to a claim by the ATO under a Director Penalty Notice if they can establish that:

- Due to illness or another acceptable reason, they were not managing the company at the time the relevant time.

- They took all reasonable steps to ensure the company paid PAYG Tax, GST or superannuation.

- They took all reasonable steps, to wind the company up or appoint a voluntary administrator .

- Reasonable steps were taken to ensure that the company complied with its obligations to pay superannuation. This defence may be available where directors reasonably thought they were engaging a subcontractor. However, the subcontractor was subsequently deemed to be an employee to which superannuation provisions applied.

Director Penalty Notices – Further Information and Advice

Given the serious consequences a Director Penalty Notice may have it is important that you urgently obtain advice if your company is unable to pay PAYG Tax, GST or superannuation.

If you need assistance, please contact our Brisbane or Gold Coast office. We will be able to advise how we can assist you in an initial obligation free consultation.